Abstract

This article aims to determine the factors that influence the role of ICTs’ role in the interaction between financial inclusion and agricultural productivity in Senegal over the period 2008-2022. The paper use of an ARDL model to show that financial inclusion has a significant negative effect on agricultural value added in Senegal in both the short and long term. However, ICTs via mobile phones do not have a positive impact on the relationship between financial inclusion and agricultural productivity in the short term. But in the long term, they improve the relationship between financial inclusion and agricultural productivity in Senegal. Agricultural land influences positively the agricultural value added in the long term, but negatively in the short term. As for the interaction between the financial inclusion index and mobile phone use, it contributes positively to Senegal's agricultural production, both in the short and long term. Therefore, to promote agricultural productivity in Senegal, the government must establish a financial system tailored to farmers' needs. It must also strengthen mobile infrastructure and promote financial inclusion through mobile telephony to enable greater use of mobile financial services, especially in rural areas. Regarding access to land resources, the Senegalese government must develop more agricultural land to improve agricultural productivity, which will in turn positively impact financial inclusion, productivity, and agricultural value added.

Keywords

Financial Inclusion, Agricultural Value Added, ICT

1. Introduction

In developing economies in sub-Saharan Africa, agriculture is a powerful lever for accelerating inclusive growth and reducing inequality. It remains the most important source of income for the majority of poor households. In Senegal, agriculture is a vital sector of the national economy and plays a significant role in food security, thus contributing to the regulation of the country's macroeconomic and social balances. Given its importance in job creation, poverty reduction, combating social inequality, and income redistribution

| [8] | De Janvry, A., & Sadoulet, E. (2010). Agricultural growth and poverty reduction: Additional evidence. The World Bank Research Observer, 25(1), 1-20.

https://doi.org/10.1093/wbro/lkp015 |

| [9] | Diallo, A., Mbaye, BB, & Thiaw, K. (2013). Agricultural productivity, economic growth and poverty in Senegal: Analysis by a recursive dynamic CGE microsimulation. Directorate of Forecasting and Economic Studies, Senegal. |

| [28] | Swinnen, J. (2016). The Political Economy of Agricultural and Food Policies. Palgrave Macmillan.

https://doi.org/10.1057/978-1-137-50102-8 |

| [29] | Thirtle, C., Lin, L., & Piesse, J. (2003). The impact of research-led agricultural productivity growth on poverty reduction in Africa, Asia and Latin America. World Development, 31(12), 1959-197. https://doi.org/10.1016/j.worlddev.2003 |

[8, 9, 28, 29]

, agriculture remains a crucial sector upon which the economies of developing countries partly depend. However, despite its importance with a contribution of 17% to Senegal's GDP

| [3] | ANSD (National Agency for Statistics and Demography). (2022). National Accounts of Senegal 2021–2022. Dakar: ANSD. |

[3]

, major challenges remain, particularly regarding the availability of financial services for rural agricultural actors.

However, despite its strategic importance, the sector faces persistent structural constraints, notably limited access to financial services tailored to the needs of farmers. Recent studies emphasize the crucial role of financial inclusion and digitalization in strengthening productivity, agricultural investment, and market integration

| [7] | Demirgüç-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2022). The Global Findex Database 2021: Financial inclusion, digital payments, and resilience in the age of COVID-19. Washington, DC: World Bank.

https://dx.doi.org/10.1596/978-1-4648-1897-4 |

| [13] | GSMA. (2023). State of the Industry Report on Mobile Money 2023. London: GSM Association. |

| [27] | Suri, T., & Jack, W. (2016). The long-run poverty and gender impacts of mobile money. Science, 354(6317), 1288-1292. https://doi.org/10.1126/science.aah5309 |

[7, 13, 27]

.

Finance, as a catalyst for modern agriculture, enables producers to invest in modern agricultural technologies, improve their practices, and better manage risks. It is now recognized as a central lever for agricultural transformation, facilitating productive investment, the adoption of technological innovations, and the management of climate and market risks

| [11] | FAO (Food and Agriculture Organization of the United Nations). (2023). The State of Food and Agriculture 2023. Rome: FAO. |

| [20] | OECD. (2023). Financing sustainable agriculture and food systems. Paris: OECD Publishing. |

| [31] | World Bank. (2022). World Development Report 2022: Finance for an equitable recovery. Washington, DC: World Bank. |

[11, 20, 31]

. In this context, financial inclusion is a mechanism that seeks to provide poor populations with easy access to formal services, ensuring their availability and accessibility at low cost

. Indeed, improved access to credit, insurance, and other financial products would allow agricultural producers to modernize their equipment, adopt sustainable farming practices, and improve their working conditions and economic well-being. Information and communication technologies (ICTs) play a crucial role in this process by offering tailored solutions to overcome traditional barriers to accessing credit. They can also help farmers improve their agricultural practices, address environmental risks, and contribute to poverty reduction in rural areas. Thus, improved financial inclusion can play a crucial role in optimizing agricultural productivity by facilitating farmers' access to fast and flexible financing to increase their yields. Furthermore, ICTs, particularly digital finance and mobile telephony, play a key role in expanding access to financial services by reducing transaction costs and information asymmetries

. They also contribute to the dissemination of agricultural, climate, and market information, strengthening farmers' capacity to manage environmental risks and optimize their production decisions. Thus, the joint development of financial inclusion and ICTs appears as a key factor in the sustainable improvement of agricultural productivity and the reduction of rural poverty.

In this context, the question that arises is what role information and communication technologies (ICTs) can play in the relationship between financial inclusion and agricultural productivity in Senegal?

The objective of our research is to analyze the effect of ICTs on the relationship between financial inclusion and agricultural productivity in Senegal. Specifically, it aims to:

1) Analyze the effect of financial inclusion on agricultural productivity in Senegal;

2) Analyze the effect of information and communication technologies on the relationship between financial inclusion and agricultural productivity in Senegal.

The remainder of this article will be organized into three parts. We will first present the literature review, then the methodological approach, and finally the results of the econometric estimations, before the conclusion and recommendations for economic policies.

2. Theoretical Framework and Literature Review

Financial inclusion is defined as “the permanent access of populations to a diverse range of appropriate financial products and services at affordable costs and used effectively, efficiently, and effectively”

| [5] | BCEAO. (2018). Annual report on the situation of financial inclusion in the WAEMU for the year 2018. |

[5]

. It involves financial innovations such as promoting microfinance and the use of electronic payment methods. The correlation between financial inclusion and agricultural productivity has been the subject of both theoretical and empirical research.

Theoretically, studies have demonstrated the importance of financial inclusion in improving agricultural productivity by facilitating access to financial resources

| [6] | Bruhn, M., & Love, I. (2014). The real impact of improved access to finance: Evidence from Mexico. The Journal of Finance, 69 (3), 1347-1376. https://doi.org/10.1111/jofi.12091 |

| [12] | Fowowe, B. (2020). The effects of financial inclusion on agricultural productivity in Nigeria. Journal of Economics and Development, 22(1), 61-79.

https://doi.org/10.1108/JED-11-2019-0059 |

| [18] | Money, U. (2014). Bank credit and agricultural development: Does it promote entrepreneurship performance? International Journal of Business and Social Science, 5, 102-107.

https://doi.org/10.30845/ijbss |

[6, 12, 18]

. Indeed, improved access to credit and savings enables the purchase of agricultural inputs necessary to increase agricultural productivity. This productivity is crucial for the socio-economic development of developing countries. However, limited access to financial resources and farmers' capacity to cope with climatic and economic risks remain major challenges. Faced with these obstacles, information and communication technologies (ICTs) appear to be a determining factor in overcoming them. Therefore, they are essential for improving agricultural producers' access to financial services. Numerous studies have shown that ICTs, through the expansion of mobile phone and internet services, have improved the level of financial inclusion

. They can also reduce access and transaction costs, particularly in remote areas

. Financial inclusion, facilitated by ICTs, can improve access to financial services such as credit, savings, and insurance

| [14] | Hossain, M., & Samad, H. (2021). Mobile phones, household welfare, and women's empowerment: Evidence from rural off-grid regions of Bangladesh. Information Technology for Development, 27(2), 191-207.

https://doi.org/10.1080/02681102.2020.1818542 |

| [16] | Loaba, S. (2022). The impact of mobile banking services on saving behavior in West Africa. Global Finance Journal, 53, 100620. https://doi.org/10.1016/j.gfj.2021.100620 |

[14, 16]

and, enabling farmers to purchase agricultural inputs needed to increase agricultural productivity and manage risks. ICTs, such as mobile phones, thus stimulate financial inclusion and contribute to reducing poverty and income inequality

| [24] | Shaikh, A. A., Alamoudi, H., Alharthi, M., & Glavee -Geo, R. (2023). Advances in mobile financial services: A review of the literature and future research directions. International Journal of Bank Marketing, 41(1), 1-33.

https://doi.org/10.1108/IJBM-06-2021-0230 |

[24]

. For example, in Kenya, the use of M-Pesa has allowed users, including farmers, to make payments, send money, and access credit via their mobile phones

. This is a significant asset for rural development.

Empirically, several studies have been conducted to assess the impact of financial inclusion on agricultural development in developing countries. Analyzing the short- and long-term dynamics of the relationship between financial inclusion and agriculture, Evans

shows that the use of financial services contributes significantly to agricultural development in both the short and long term. Agbenyo, Jiang, and Antony

| [1] | Agbenyo, W., et al. (2019). Cointegration analysis of agricultural growth and financial inclusion in Ghana. Theoretical Economics Letters, 9, 895-911.

https://doi.org/10.4236/tel.2019.94058 |

[1]

, using the FMOLS estimation method, demonstrated that financial inclusion through domestic credit to the private sector negatively and significantly affects agricultural growth, while through interest rates, it positively and significantly affects agricultural growth in Ghana. Napo

| [19] | Napo, F. (2019). Financial inclusion and agricultural exports of WAEMU countries: the role of institutional quality. MPRA Paper 94203, University Library of Munich.

https://mpra.ub.uni-muenchen.de/94203/ |

[19]

, using the generalized method of moments, analyzed the role of institutional quality in the relationship between financial inclusion and agricultural exports from WAEMU countries. The results of his estimations show a positive effect of financial inclusion on agricultural exports. This study also highlights that financial inclusion indicators affect agricultural exports from WAEMU countries through the channel of improved institutional quality. Furthermore, Akpa et al.

, using ordinary least squares (OLS), demonstrate a positive and significant impact of access to financial services on agricultural production in Benin, while the use of financial services has a positive but not significant impact on agricultural production in that country.

M. Toure et al.

| [17] | Malick Toure et al. (2023). Dynamique de l’inclusion financière et développement agricole dans les pays de l’UEMOA [Dynamics of financial inclusion and agricultural development in WAEMU countries]. Journal of Academic Finance. Article. Vol. 14 No. 2 (2023): Fall 2023.

https://doi.org/10.59051/joaf.v14i2.688 |

[17]

analyze the effect of financial inclusion on agricultural development in WAEMU countries over the period 2000–2020. In this study, agricultural development is represented by the agricultural production index and financial inclusion by two variables: the rate of microfinance service utilization and the rate of banking service utilization (based on the adult population: 15 years and older). Using the generalized method of moments in a system, the authors showed that the use of microfinance services, the productive capacity index, and arable land contribute significantly to improving the agricultural production index. Using the same estimation method as M. Toure et al.

| [17] | Malick Toure et al. (2023). Dynamique de l’inclusion financière et développement agricole dans les pays de l’UEMOA [Dynamics of financial inclusion and agricultural development in WAEMU countries]. Journal of Academic Finance. Article. Vol. 14 No. 2 (2023): Fall 2023.

https://doi.org/10.59051/joaf.v14i2.688 |

[17]

, Patrick Arnold Ombiono Kitoto

| [22] | Patrick Arnold Ombiono Kitoto ((2024), Digital Financial Inclusion and Agricultural Productivity. Evidence from Sub-Saharan Africa. In Financer les transformations agricoles et alimentaires. Revue Internationale des Études du Développement. [Financing agricultural and food transformations. International Review of Development Studies]. p. 89-116.

https://doi.org/10.4000/ried.10245 |

[22]

investigated the effect of digital financial inclusion on agricultural productivity in sub-Saharan Africa during the period 2015–2020. To this end, partial land productivity (PLP) was used to measure agricultural productivity, and access to and use of mobile money services for digital financial inclusion (DFI) was analyzed. The results of the analyses show that DFI significantly affects PLP growth. These findings suggest that promoting digital financial services tailored to farmers' needs can stimulate agricultural transformation in sub-Saharan Africa.

During the same period, Vangvaidi, A., & Gramtya Djidda, L.

| [30] | Vangvaidi, A., & Gramtya Djidda, L. (2024). Inclusive finance and agricultural growth in sub-Saharan Africa: The role of ICTs. International Journal of Accounting, Finance, Auditing, Management and Economics, 5(8), 95-111.

https://doi.org/10.5281/zenodo.13328513 |

[30]

analyze the role of ICTs in the relationship between inclusive finance and agricultural growth over the period from 2004 to 2020. To achieve this objective, the authors measured information and communication technologies using the mobile phone variable and financial inclusion through indicators of access to and use of financial services. The results of the study showed that inclusive finance positively affects agricultural growth in sub-Saharan Africa through ICT channels. Furthermore, the authors suggest strengthening mobile phone use to facilitate access to and use of financial services for people whose livelihoods depend on agriculture in sub-Saharan Africa.

In summary, the literature on the relationship between financial inclusion and agricultural productivity presents mixed opinions. Some studies show a positive and significant effect of financial inclusion on agricultural productivity

. While others show a negative effect of financial inclusion on agricultural productivity

| [21] | Onoja, John J. (2017), "Financial Sector Development and Agricultural Productivity". Master's Theses. 238. https://repository.usfca.edu/thes/238 |

| [30] | Vangvaidi, A., & Gramtya Djidda, L. (2024). Inclusive finance and agricultural growth in sub-Saharan Africa: The role of ICTs. International Journal of Accounting, Finance, Auditing, Management and Economics, 5(8), 95-111.

https://doi.org/10.5281/zenodo.13328513 |

[21, 30]

.

3. Methodology and Model Specification

3.1. Model Specification

This section focuses on the specification of the study model and the definition of the variables, as well as their evolution, are outlined. The methodology adopted here aims to analyze the impact of information and communication technologies on the relationship between financial inclusion and agricultural productivity in Senegal. To this end, econometric estimations are made using the ARDL " Auto-Regressive " model Distributed Cointegration lag

| [23] | Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289-326.

https://doi.org/10.1002/jae.616 |

[23]

, in order to analyze the short-term and long-term relationships between variables through the following relationship:

Or

1) VAA is the agricultural value added as a percentage of GDP;

2) IIF, the Financial Inclusion Index;

3) TELM the number of individuals using mobile phones as a percentage of the total population;

4) IIF*TELM represents the interaction between the financial inclusion index and the number of individuals using mobile phones;

5) TA represents agricultural land as a percentage of the territory's area.

6) Up to represents the coefficients of the variables to be estimated in the long term and, , , represents the coefficients of the variables to be estimated in the short term;

7) Indicates the constant and the random error term at time t.

8) Δ is the first difference operator, log is the logarithm, and p, q, r, s, t represent the optimal number of delays.

3.2. Methodological Tools

Before estimating the model, we will first verify the stationarity of the data, the validity of the model, and the existence of a long-term relationship. For the stationarity test, we will use the Augmented Dickey -Fuller test. This test determines whether a time series is stationary or not. The decision rule is as follows:

1) If the p-value is less than the threshold (often 1%, 5%, 10%), then we reject the null hypothesis of the presence of a unit root. We conclude that the series is stationary;

2) If the p-value is greater than the threshold (often 1%, 5%, 10%), the null hypothesis of a unit root is not rejected. The series is concluded to be non-stationary.

Regarding the validity of the model, we will perform the Jarque-Bara normality test, the autocorrelation test, the heteroscedasticity test and the stability test of the coefficients.

The Jarque-Bera normality test is used to verify the normality of a statistical distribution. The decision rule involves comparing the p-value to the chosen threshold (1%, 5%, 10%). For example, if the p-value is greater than 5%, then the null hypothesis of normality of the data is not rejected. This means that the variables follow a normal distribution.

Durbin Watson, White and Cusum tests will be used to detect autocorrelation of errors, heteroscedasticity and stability of coefficients respectively.

To verify the existence of a long-term relationship between the variables, we will use the bounds test of Pesaran et al

| [23] | Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289-326.

https://doi.org/10.1002/jae.616 |

[23]

. The decision rule of this method consists of comparing the F- statistic to the critical values of the lower (I(0)) and upper (I(1)) bounds.

1) If the statistical value of F obtained is greater than the value of the upper bound, then the null hypothesis is rejected. Therefore, a long-term relationship exists.

2) If the statistical value of F obtained is less than the value of the lower bound, then the null hypothesis is not rejected. Therefore, there is no long-term relationship.

3) If the statistical value of F obtained is between the two bounds, then the test does not allow us to conclude.

The study data covers the period 2008-2022 and comes from two sources, namely the reports on the state of financial inclusion in the WAEMU for the years 2018 and 2022 and the World Bank database (WDI)

| [31] | World Bank. (2022). World Development Report 2022: Finance for an equitable recovery. Washington, DC: World Bank. |

[31]

.

4. Data Analysis

4.1. Definitions and Evolution of Variables During the Period 2008 – 2022

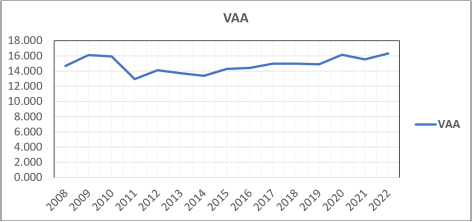

Agricultural value added: This represents the dependent variable of the study, which measures the level of agricultural productivity in Senegal. Its evolution over the period 2008 to 2022 is shown in

Figure 1 below. Analysis of this graph shows a decrease in agricultural value added over the period 2008–2011, falling from 14.687% in 2008 to 12.947% in 2011, a decrease of 1.74%. This situation can be explained by the decrease in rainfall observed in 2011. On the other hand, the VAA increased over the period from 2011 to 2022, rising from 12.947% in 2011 to 16.341% in 2022. This upward trend can be attributed to several factors such as favorable climatic conditions and agricultural development programs like the Emerging Senegal Plan (PSE) and the agricultural development hubs (PDA).

Figure 1. Evolution of agricultural value added in Senegal.

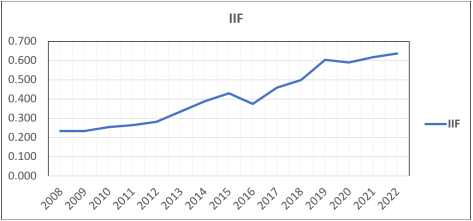

Financial inclusion: In this study, it is measured by the financial inclusion index, which ranges from 0 to 1, where 0 represents total exclusion and 1 represents successful financial inclusion. According to the

Figure 2 below, Senegal's financial inclusion index increased by 0.403 points between 2008 and 2022, rising from 0.233 to 0.636. This improvement is explained by the progress in indicators related to access to and use of financial services.

Figure 2. Changes in Senegal's financial inclusion index.

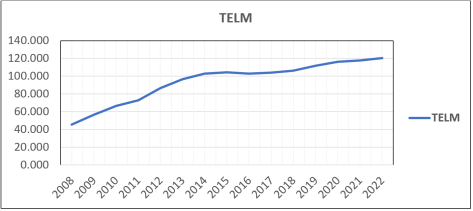

Number of mobile phone users: this is the indicator chosen in this study to measure the level of information and communication technologies in Senegal. According to the

Figure 3 below, Senegal recorded a 75.044% increase in the number of mobile phone users, reaching 120.434% in 2022 compared to 45.39% in 2008. This growth could be explained by the expansion of network coverage and adaptation to social needs. It can also be explained by increased access to financial services via mobile.

Figure 3. Evolution of the number of mobile phone users in Senegal.

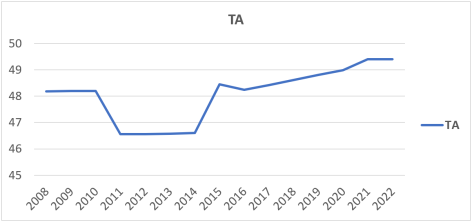

Agricultural land (percentage of the territory): refers to access to land resources. The

Figure 4 below shows a decrease in access to land resources between 2008 and 2014. Following this downward trend, observed since 2008, access to land resources increased between 2014 and 2022, reaching 49.4% in 2022, compared to 46.601% in 2014. This situation is partly explained by the implementation of certain agricultural projects such as the Program for Accelerating the Pace of Senegalese Agriculture (PRACAS) and the rice self-sufficiency program.

Figure 4. Evolutions agricultural land in Senegal.

4.2. Econometric Results and Discussion

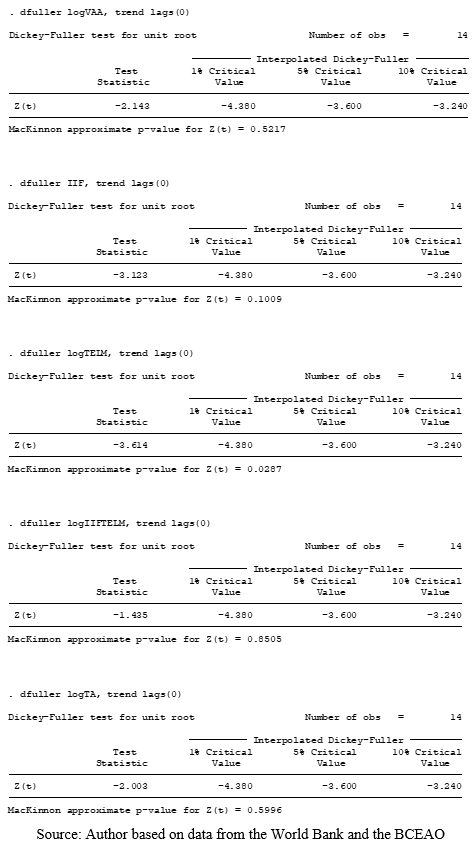

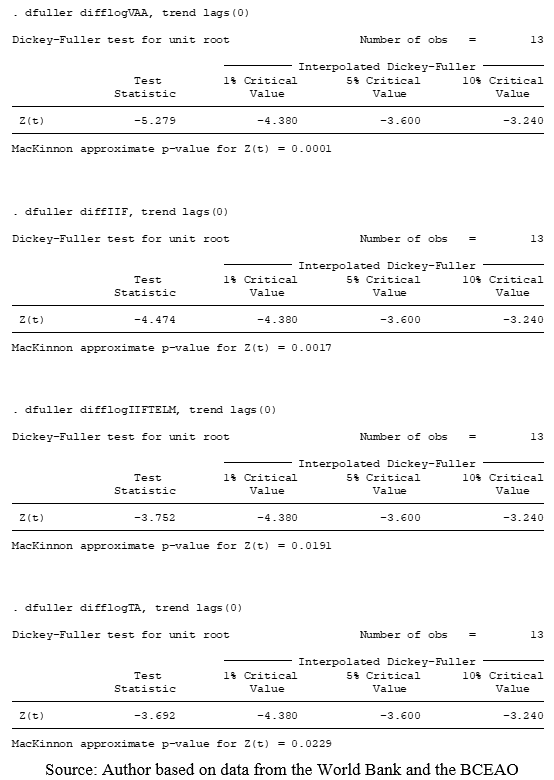

4.2.1. Stationarity Test

Dickey -Fuller test was used to test the stationarity of the data. The results (

Table 1) show that the variables agricultural value added, financial inclusion index, interaction between the financial inclusion index and mobile phone use, and agricultural land are stationary in first differences (I(1)), while mobile phone use is stationary in I(0) at the 5% significance level. The variables are integrated at different orders (I(0) and I(1)), which demonstrates that the ARDL model is applicable.

Table 1. Stationarity test results.

Variables | Statistical Test | Prob. | 1% Critical Value | 5% Critical Value | 10% Critical Value | Conclusion |

VAA | -5,279 | 0.0001 | -4.38 | -3.6 | -3.24 | I (1) |

IIF | -4,474 | 0.0017 | -4.38 | -3.6 | -3.24 | I (1) |

TELM | -3.614 | 0.0287 | -4.38 | -3.6 | -3.24 | I (0) |

IIF*TELM | -3.752 | 0.0191 | -4.38 | -3.6 | -3.24 | I (1) |

YOUR | -3.692 | 0.0229 | -4.38 | -3.6 | -3.24 | I (1) |

Source: Author based on data from the World Bank and the BCEAO

Note: I(1) represents the stationary variables in first difference and I(0) the stationary one in level.

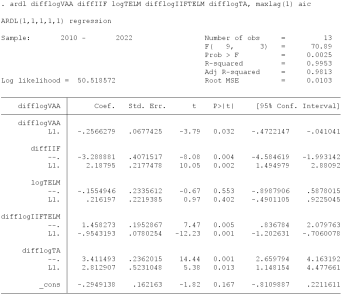

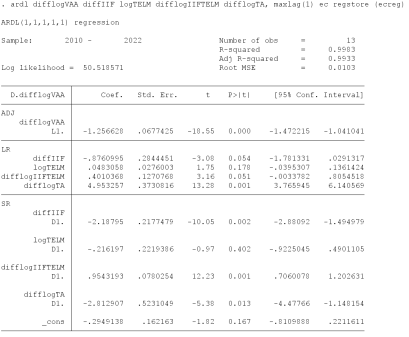

The results in

Table 2 show, through the F- statistic value and its probability, that the model is globally significant. They also show that 99.53% of the fluctuations in agricultural value added are explained by the variables. The Akaike Information Criterion (AIC) is used to select the optimal ARDL model.

Table 2. Results of the ARDL (1,1,1,1) model estimation.

Variables | Coefficient | Std. Error | t - Statistics | Prob. |

VAA | | | | |

L1. | -0.2566279 | 0.0677425 | -3.79 | 0.032 |

IIF | -3.288881 | 0.4071517 | -8.08 | 0.004 |

L1. | 2.18795 | 0.2177478 | 10.05 | 0.002 |

TELM | -0.1554946 | 0.2335612 | -0.67 | 0.553 |

L1. | 0.216197 | 0.2219385 | 0.97 | 0.402 |

IIF*TELM | 1,458273 | 0.1952867 | 7.47 | 0.005 |

L1. | -0.9543193 | 0.0780254 | -12.23 | 0.001 |

YOUR | 3,411493 | 0.2362015 | 14.44 | 0.001 |

L1. | 2.812907 | 0.5231048 | 5.38 | 0.013 |

Const | -0.2949138 | 0.162163 | -1.82 | 0.167 |

F- statistic | 70.89 |

R- squared | 0.9953 |

Prob > F | 0.0025 |

Source: Author based on data from the World Bank and the BCEAO

Note: L1 refers to the lagged value of each variable.

4.2.2. Model Validity Test

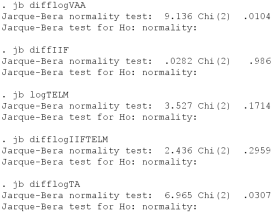

Furthermore, the validity of our model was examined using the Jarque-Bara normality test. Through the results in

Table 3, we observed that the probabilities associated with the Jarque statistical test Bera values are greater than 5% except for the variables VAA and TA. However, the latter are greater than 1%, which indicates that all variables follow a normal distribution.

Table 3. Jarque Bera Normality Test.

Variables | Statistics | Prob |

VAA | 9,136 | 0.0104 |

IIF | 0.0282 | 0.986 |

TELM | 3,527 | 0.1714 |

IIF*TELM | 2,436 | 0.2959 |

YOUR | 6,965 | 0.0307 |

Source: Author based on data from the World Bank and the BCEAO

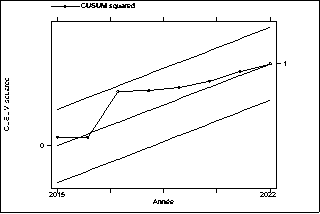

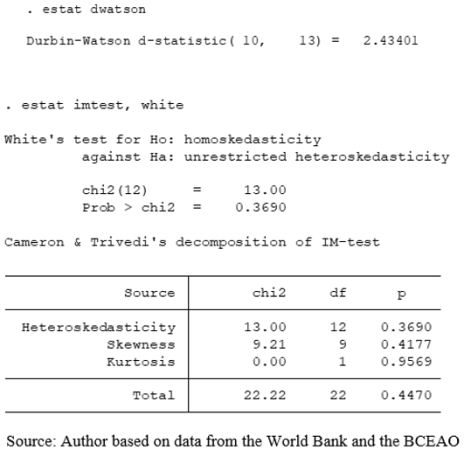

Furthermore, the Durbin Watson autocorrelation test (2.43401) and the White heteroscedasticity test (0.3690) showed no autocorrelation of the residuals and no heteroscedasticity of the errors, respectively. Finally, the Cusum test (

Figure 5) indicates that all coefficients are stable during the analysis period, as the residuals remain within the 5% confidence interval. Ultimately, these results allow us to conclude that the model is valid.

Figure 5. Cusum test results.

4.2.3. Cointegration Test

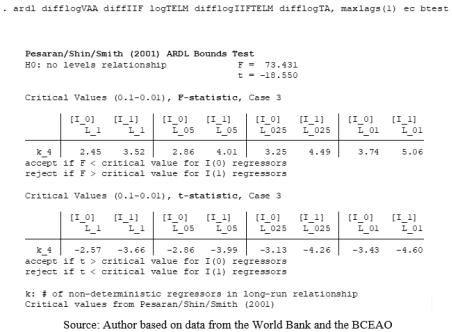

cointegration test using the bounds approach of Pesaran et al

| [29] | Thirtle, C., Lin, L., & Piesse, J. (2003). The impact of research-led agricultural productivity growth on poverty reduction in Africa, Asia and Latin America. World Development, 31(12), 1959-197. https://doi.org/10.1016/j.worlddev.2003 |

[29]

presented in the table below show the existence of a long-term equilibrium relationship between the variables of the model.

Table 4. Results of the bounds test.

Test Statistic Value |

F- statistic 73,431 |

K 4 |

Signif. I (0) I (1) |

10% 2.45 3.52 |

5% 2.86 4.01 |

2.5% 3.25 4.49 |

1% 3.74 5.06 |

Source: Author based on data from the World Bank and the BCEAO

4.2.4. Short-term Dynamics

Table 5. Coefficients of the short-term relationship.

Variables | Coefficient | Std. Error | Prob. |

IIF | -2.18795** | 0.2177479 | 0.002 |

TELM | -0.216197 | 0.2219386 | 0.402 |

IIF*TELM | 0.9543193** | 0.0780254 | 0.001 |

YOUR | -2.812907** | 0.5231049 | 0.013 |

CointEq (-) | -1.256628 ** | 0.0677425 | 0.000 |

Source: Author based on data from the World Bank and the BCEAO

Note: * P < 1%, ** p < 5%, *** P < 10%

According to the results in

Table 5, financial inclusion has a significant negative impact on agricultural value added in Senegal in the short term, meaning that the level of financial inclusion remains insufficient to stimulate agricultural production in Senegal. This result can also be explained by structural and environmental problems such as the climate and the country's agricultural policy. Consequently, even if farmers receive financing, these external factors may limit the impact of this financing on agricultural productivity.

Regarding mobile phone usage, it negatively impacts agricultural production in Senegal. This means that in the short term, a 1% increase in the number of mobile phone users implies a 0.216% decrease in Senegal's agricultural value added.

Regarding the interaction variable between the financial inclusion index and mobile phone use, it shows a positive and significant effect on Senegal's agricultural value added. This implies that a 1% increase in the level of financial inclusion through mobile phones leads to a 0.954% increase in Senegal's agricultural value added. This result demonstrates that the impact of financial inclusion on Senegal's agricultural value-added increases with the number of mobile phone users. In other words, it positively impacts the country's agricultural productivity when there is a significant number of mobile phone users.

Regarding the variable access to land resources (TA), it has a negative and significant effect on agricultural production in Senegal.

Furthermore, the error correction coefficient is negative and highly significant. Therefore, short-term imbalances correct themselves in the long term.

4.2.5. Long-term Dynamics

The results of the long-term coefficient estimation presented in the table below show the significant negative effect of the financial inclusion index on agricultural value added in Senegal, indicating that the level of financial inclusion remains insufficient to stimulate agricultural production in the country. While financial inclusion negatively impacts agricultural value added in both the short and long term, this impact is less pronounced in the short term.

The coefficient for the mobile phone variable is positive but not significant in the long term. This means that a 1% increase in the number of mobile phone users leads to a 0.048% increase in agricultural production in the long term, all other things being equal. The variables of agricultural land and the interaction between the financial inclusion index and mobile phones showed a positive and significant effect on Senegal's agricultural value added in the long term.

Table 6. Coefficients of the long-term relationship.

Variables | Coefficient | Std. Error | Prob. |

IIF | -0.8760995 *** | 0.2844451 | 0.054 |

TELM | 0.0483058 | 0.0276003 | 0.178 |

IIF*TELM | 0.4010368 *** | 0.1270768 | 0.051 |

YOUR | 4.953257** | 0.3730816 | 0.001 |

Const | -0.2949138 | 0.162163 | 0.167 |

Source: Author based on data from the World Bank and the BCEAO

Note: * P < 1%, ** p < 5%, *** P < 10%

Overall, the test results showed a negative effect of financial inclusion on agricultural productivity in Senegal in both the short and long term. However, ICTs, particularly mobile phones, negatively impact the relationship between financial inclusion and agricultural productivity in Senegal in the short term, but positively in the long term.

5. Conclusion and Implications of Economic Policies

The objective of our research was to analyze the impact of information and communication technologies on the relationship between financial inclusion and agricultural productivity in Senegal over the period 2008-2022. To this end, the Dickey -Fuller stationarity test, the Jarque - Bera normality test, the Durbin- Watson autocorrelation test, the White heteroscedasticity test, and the ARDL cointegration model of Pesaran et al.

| [23] | Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289-326.

https://doi.org/10.1002/jae.616 |

[23]

were used. The results of the latter estimation showed that financial inclusion has a significant negative effect on agricultural value added in Senegal in both the short and long term. Therefore, a 1% increase in financial inclusion leads to a decrease in agricultural value added in Senegal of 2.188% in the short term and 0.876% in the long term. However, ICTs via mobile phones do not have a positive impact on the relationship between financial inclusion and agricultural productivity in the short term. But in the long term, they improve the relationship between financial inclusion and agricultural productivity in Senegal. This means that in the long term, any increase in the number of mobile phone users would lead to an increase in agricultural productivity in Senegal.

Regarding the variable of agricultural land, it positively influences Senegal's agricultural value added in the long term, but negatively in the short term. This means that in the long term, any increase in agricultural land would lead to an increase in Senegal's agricultural value added, while in the short term, any increase in agricultural land would lead to a decrease in Senegal's agricultural value added. As for the interaction between the financial inclusion index and mobile phone use, it contributes positively to Senegal's agricultural production, both in the short and long term. Consequently, a 1% increase in the level of financial inclusion through mobile phone use leads to a 0.954% increase in the short term and a 0.401% increase in the long term of agricultural value added in Senegal.

Therefore, to promote agricultural productivity in Senegal, the government must establish a financial system tailored to farmers' needs. It must also strengthen mobile infrastructure and promote financial inclusion through mobile telephony to enable greater use of mobile financial services, especially in rural areas. Regarding access to land resources, the Senegalese government must develop more agricultural land to improve agricultural productivity, which will in turn positively impact financial inclusion, productivity, and agricultural value added.

Abbreviations

AIC | Akaike Information Criterion |

ANSD | Agence nationale de la statistique et de la démographie (National Agency for Statistics and Demography) |

ARDL | Autoregressive Distributed Lag Models |

BCEAO | Banque Centrale des États de l'Afrique de l'Ouest (BCEAO) - Central Bank of West African States (BCEAO) |

DFI | Digital Financial Inclusion |

FAO | Food and Agriculture Organization |

FMOLS | Fully Modified Ordinary Least Squares |

GDP | Gross Domestic Product (GDP) |

GSMA | Global System for Mobile Association (GSMA) |

ICT | Information and Communication Technology |

IIF | Financial Inclusion Index |

OECD | Organisation for Economic Co-operation and Development) |

OLS | Ordinary Least Squares |

PDA | Agricultural Development Hubs |

PRACAS | Programme for Accelerating the Pace of Senegalese Agriculture |

PSE | Emerging Senegal Plan |

VAA | Agricultural Value Added |

WAEMU | West African Economic and Monetary Union (WAEMU) |

WDI | World Bank Indicators |

Author Contributions

Mohamed Ben Omar Ndiaye: Conceptualization, Data curation, Formal Analysis, Methodology, Validation, Writing – original draft, Writing – review & editing

Ousmane Diouf: Conceptualization, Data curation, Formal Analysis, Methodology, Writing – original draft

Papa Mallé Ndiaye: Data curation, Formal Analysis, Methodology, Supervision, Writing – original draft, Writing – review & editing

Conflicts of Interest

The authors declare no conflict of interest.

Appendix

Appendix I: Study Data

Table 7. Study Data.

Year | VAA | IIF | TELM | IIF*TELM | YOUR |

2008 | 14,687 | 0.233 | 45,390 | 10,576 | 48,174 |

2009 | 16,108 | 0.233 | 56,593 | 13,186 | 48,190 |

2010 | 15,945 | 0.253 | 66,589 | 16,847 | 48,190 |

2011 | 12,947 | 0.264 | 72,639 | 19,177 | 46,564 |

2012 | 14,098 | 0.281 | 86,690 | 24,360 | 46,564 |

2013 | 13,725 | 0.334 | 96,603 | 32,265 | 46,580 |

2014 | 13,369 | 0.388 | 102,931 | 39,937 | 46,601 |

2015 | 14,283 | 0.430 | 104,202 | 44,807 | 48,450 |

2016 | 14,414 | 0.375 | 102,950 | 38,606 | 48,242 |

2017 | 14,982 | 0.459 | 103,962 | 47,719 | 48,424 |

2018 | 14,988 | 0.499 | 106,324 | 53,056 | 48,605 |

2019 | 14,896 | 0.604 | 111,748 | 67,496 | 48,798 |

2020 | 16,149 | 0.589 | 116,079 | 68,371 | 48,979 |

2021 | 15,551 | 0.618 | 117,677 | 72,724 | 49,400 |

2022 | 16,341 | 0.636 | 120,434 | 76,596 | 49,400 |

Source: Author based on data from the World Bank and the BCEAO

Appendix II: Stationarity Test

Figure 6. Stationary test in level.

Figure 7. Stationary test in first difference.

Appendix III: Estimation of the ARDL (1,1,1,1,1) Model

Figure 8. Estimation of the ARDL Model.

Appendix IV: Jarque-Bera Normality

Figure 9. Jarque-Bera Normality test.

Appendix V: Cointegration Test

Figure 10. Cointegration test.

Appendix VI: Short and Long-Term Dynamics

Figure 11. Short and Long-Term Dynamics test.

Appendix VII: Durbin Watson's Autocorrelation Test and White's Heteroscedasticity Test

Figure 12. Durbin Watson's Autocorrelation Test and White's Heteroscedasticity Test.

References

| [1] |

Agbenyo, W., et al. (2019). Cointegration analysis of agricultural growth and financial inclusion in Ghana. Theoretical Economics Letters, 9, 895-911.

https://doi.org/10.4236/tel.2019.94058

|

| [2] |

Akpa, A., Chabossou, A., & Degbedji, DF (2021). Effect of financial inclusion on agricultural growth in Benin. Les Annales des Sciences Économiques de l'UAC [The Annals of Economic Sciences of the UAC] 2(2), 1-16.

https://www.researchgate.net/publication/349624488_Effet_de_l'inclusion_financiere_sur_la_croissance_agricole_au_Benin

|

| [3] |

ANSD (National Agency for Statistics and Demography). (2022). National Accounts of Senegal 2021–2022. Dakar: ANSD.

|

| [4] |

Aron, J. (2018). Mobile money and the economy: A review of the evidence. The World Bank Research Observer, 33, 135-188.

https://doi.org/10.1093/wbro/lky001

|

| [5] |

BCEAO. (2018). Annual report on the situation of financial inclusion in the WAEMU for the year 2018.

|

| [6] |

Bruhn, M., & Love, I. (2014). The real impact of improved access to finance: Evidence from Mexico. The Journal of Finance, 69 (3), 1347-1376.

https://doi.org/10.1111/jofi.12091

|

| [7] |

Demirgüç-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2022). The Global Findex Database 2021: Financial inclusion, digital payments, and resilience in the age of COVID-19. Washington, DC: World Bank.

https://dx.doi.org/10.1596/978-1-4648-1897-4

|

| [8] |

De Janvry, A., & Sadoulet, E. (2010). Agricultural growth and poverty reduction: Additional evidence. The World Bank Research Observer, 25(1), 1-20.

https://doi.org/10.1093/wbro/lkp015

|

| [9] |

Diallo, A., Mbaye, BB, & Thiaw, K. (2013). Agricultural productivity, economic growth and poverty in Senegal: Analysis by a recursive dynamic CGE microsimulation. Directorate of Forecasting and Economic Studies, Senegal.

|

| [10] |

Evens, O. (2017). Back to the land: The impact of financial inclusion on agriculture in Nigeria. Iranian Economic Review, 21(4), 885-903.

https://doi.org/10.22059/ier.2017.64086

|

| [11] |

FAO (Food and Agriculture Organization of the United Nations). (2023). The State of Food and Agriculture 2023. Rome: FAO.

|

| [12] |

Fowowe, B. (2020). The effects of financial inclusion on agricultural productivity in Nigeria. Journal of Economics and Development, 22(1), 61-79.

https://doi.org/10.1108/JED-11-2019-0059

|

| [13] |

GSMA. (2023). State of the Industry Report on Mobile Money 2023. London: GSM Association.

|

| [14] |

Hossain, M., & Samad, H. (2021). Mobile phones, household welfare, and women's empowerment: Evidence from rural off-grid regions of Bangladesh. Information Technology for Development, 27(2), 191-207.

https://doi.org/10.1080/02681102.2020.1818542

|

| [15] |

Lenka, S., & Barik, R. (2018). Has expansion of mobile phone and internet use spurred financial inclusion in the SSAR countries? Financial Innovation.

https://doi.org/10.1186/s40854-018-0089-x

|

| [16] |

Loaba, S. (2022). The impact of mobile banking services on saving behavior in West Africa. Global Finance Journal, 53, 100620.

https://doi.org/10.1016/j.gfj.2021.100620

|

| [17] |

Malick Toure et al. (2023). Dynamique de l’inclusion financière et développement agricole dans les pays de l’UEMOA [Dynamics of financial inclusion and agricultural development in WAEMU countries]. Journal of Academic Finance. Article. Vol. 14 No. 2 (2023): Fall 2023.

https://doi.org/10.59051/joaf.v14i2.688

|

| [18] |

Money, U. (2014). Bank credit and agricultural development: Does it promote entrepreneurship performance? International Journal of Business and Social Science, 5, 102-107.

https://doi.org/10.30845/ijbss

|

| [19] |

Napo, F. (2019). Financial inclusion and agricultural exports of WAEMU countries: the role of institutional quality. MPRA Paper 94203, University Library of Munich.

https://mpra.ub.uni-muenchen.de/94203/

|

| [20] |

OECD. (2023). Financing sustainable agriculture and food systems. Paris: OECD Publishing.

|

| [21] |

Onoja, John J. (2017), "Financial Sector Development and Agricultural Productivity". Master's Theses. 238.

https://repository.usfca.edu/thes/238

|

| [22] |

Patrick Arnold Ombiono Kitoto ((2024), Digital Financial Inclusion and Agricultural Productivity. Evidence from Sub-Saharan Africa. In Financer les transformations agricoles et alimentaires. Revue Internationale des Études du Développement. [Financing agricultural and food transformations. International Review of Development Studies]. p. 89-116.

https://doi.org/10.4000/ried.10245

|

| [23] |

Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289-326.

https://doi.org/10.1002/jae.616

|

| [24] |

Shaikh, A. A., Alamoudi, H., Alharthi, M., & Glavee -Geo, R. (2023). Advances in mobile financial services: A review of the literature and future research directions. International Journal of Bank Marketing, 41(1), 1-33.

https://doi.org/10.1108/IJBM-06-2021-0230

|

| [25] |

Sarma, M. and Pais, J. (2011) Financial Inclusion and Development. Journal of International Development, 23, 613-625.

https://doi.org/10.1002/jid.1698

|

| [26] |

Suri, T. (2017). Mobile money. Annual Review of Economics, 9(1), 497-520.

https://doi.org/10.1146/annurev-economics-063016-103638

|

| [27] |

Suri, T., & Jack, W. (2016). The long-run poverty and gender impacts of mobile money. Science, 354(6317), 1288-1292.

https://doi.org/10.1126/science.aah5309

|

| [28] |

Swinnen, J. (2016). The Political Economy of Agricultural and Food Policies. Palgrave Macmillan.

https://doi.org/10.1057/978-1-137-50102-8

|

| [29] |

Thirtle, C., Lin, L., & Piesse, J. (2003). The impact of research-led agricultural productivity growth on poverty reduction in Africa, Asia and Latin America. World Development, 31(12), 1959-197.

https://doi.org/10.1016/j.worlddev.2003

|

| [30] |

Vangvaidi, A., & Gramtya Djidda, L. (2024). Inclusive finance and agricultural growth in sub-Saharan Africa: The role of ICTs. International Journal of Accounting, Finance, Auditing, Management and Economics, 5(8), 95-111.

https://doi.org/10.5281/zenodo.13328513

|

| [31] |

World Bank. (2022). World Development Report 2022: Finance for an equitable recovery. Washington, DC: World Bank.

|

Cite This Article

-

APA Style

Ndiaye, M. B. O., Diouf, O., Ndiaye, P. M. (2026). Determining Factors Influencing ICTs’ Role in the Interaction Between Financial Inclusion and Agricultural Productivity in Senegal. International Journal of Sustainable Development Research, 12(2), 85-99. https://doi.org/10.11648/j.ijsdr.20261202.11

Copy

|

Copy

|

Download

Download

ACS Style

Ndiaye, M. B. O.; Diouf, O.; Ndiaye, P. M. Determining Factors Influencing ICTs’ Role in the Interaction Between Financial Inclusion and Agricultural Productivity in Senegal. Int. J. Sustain. Dev. Res. 2026, 12(2), 85-99. doi: 10.11648/j.ijsdr.20261202.11

Copy

|

Download

AMA Style

Ndiaye MBO, Diouf O, Ndiaye PM. Determining Factors Influencing ICTs’ Role in the Interaction Between Financial Inclusion and Agricultural Productivity in Senegal. Int J Sustain Dev Res. 2026;12(2):85-99. doi: 10.11648/j.ijsdr.20261202.11

Copy

|

Download

-

@article{10.11648/j.ijsdr.20261202.11,

author = {Mohamed Ben Omar Ndiaye and Ousmane Diouf and Papa Mallé Ndiaye},

title = {Determining Factors Influencing ICTs’ Role in the Interaction Between Financial Inclusion and Agricultural Productivity in Senegal},

journal = {International Journal of Sustainable Development Research},

volume = {12},

number = {2},

pages = {85-99},

doi = {10.11648/j.ijsdr.20261202.11},

url = {https://doi.org/10.11648/j.ijsdr.20261202.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijsdr.20261202.11},

abstract = {This article aims to determine the factors that influence the role of ICTs’ role in the interaction between financial inclusion and agricultural productivity in Senegal over the period 2008-2022. The paper use of an ARDL model to show that financial inclusion has a significant negative effect on agricultural value added in Senegal in both the short and long term. However, ICTs via mobile phones do not have a positive impact on the relationship between financial inclusion and agricultural productivity in the short term. But in the long term, they improve the relationship between financial inclusion and agricultural productivity in Senegal. Agricultural land influences positively the agricultural value added in the long term, but negatively in the short term. As for the interaction between the financial inclusion index and mobile phone use, it contributes positively to Senegal's agricultural production, both in the short and long term. Therefore, to promote agricultural productivity in Senegal, the government must establish a financial system tailored to farmers' needs. It must also strengthen mobile infrastructure and promote financial inclusion through mobile telephony to enable greater use of mobile financial services, especially in rural areas. Regarding access to land resources, the Senegalese government must develop more agricultural land to improve agricultural productivity, which will in turn positively impact financial inclusion, productivity, and agricultural value added.},

year = {2026}

}

Copy

|

Download

-

TY - JOUR

T1 - Determining Factors Influencing ICTs’ Role in the Interaction Between Financial Inclusion and Agricultural Productivity in Senegal

AU - Mohamed Ben Omar Ndiaye

AU - Ousmane Diouf

AU - Papa Mallé Ndiaye

Y1 - 2026/04/10

PY - 2026

N1 - https://doi.org/10.11648/j.ijsdr.20261202.11

DO - 10.11648/j.ijsdr.20261202.11

T2 - International Journal of Sustainable Development Research

JF - International Journal of Sustainable Development Research

JO - International Journal of Sustainable Development Research

SP - 85

EP - 99

PB - Science Publishing Group

SN - 2575-1832

UR - https://doi.org/10.11648/j.ijsdr.20261202.11

AB - This article aims to determine the factors that influence the role of ICTs’ role in the interaction between financial inclusion and agricultural productivity in Senegal over the period 2008-2022. The paper use of an ARDL model to show that financial inclusion has a significant negative effect on agricultural value added in Senegal in both the short and long term. However, ICTs via mobile phones do not have a positive impact on the relationship between financial inclusion and agricultural productivity in the short term. But in the long term, they improve the relationship between financial inclusion and agricultural productivity in Senegal. Agricultural land influences positively the agricultural value added in the long term, but negatively in the short term. As for the interaction between the financial inclusion index and mobile phone use, it contributes positively to Senegal's agricultural production, both in the short and long term. Therefore, to promote agricultural productivity in Senegal, the government must establish a financial system tailored to farmers' needs. It must also strengthen mobile infrastructure and promote financial inclusion through mobile telephony to enable greater use of mobile financial services, especially in rural areas. Regarding access to land resources, the Senegalese government must develop more agricultural land to improve agricultural productivity, which will in turn positively impact financial inclusion, productivity, and agricultural value added.

VL - 12

IS - 2

ER -

Copy

|

Download